In insurance policies, insurance deductible is one terms that comes up always.” Understanding what an insurance deductible is and how it works is crucial for anyone looking to purchase insurance coverage. This article will delve into the concept of insurance deductibles, explore their significance, and discuss how they affect your insurance claims.

What Is An Insurance Deductible?

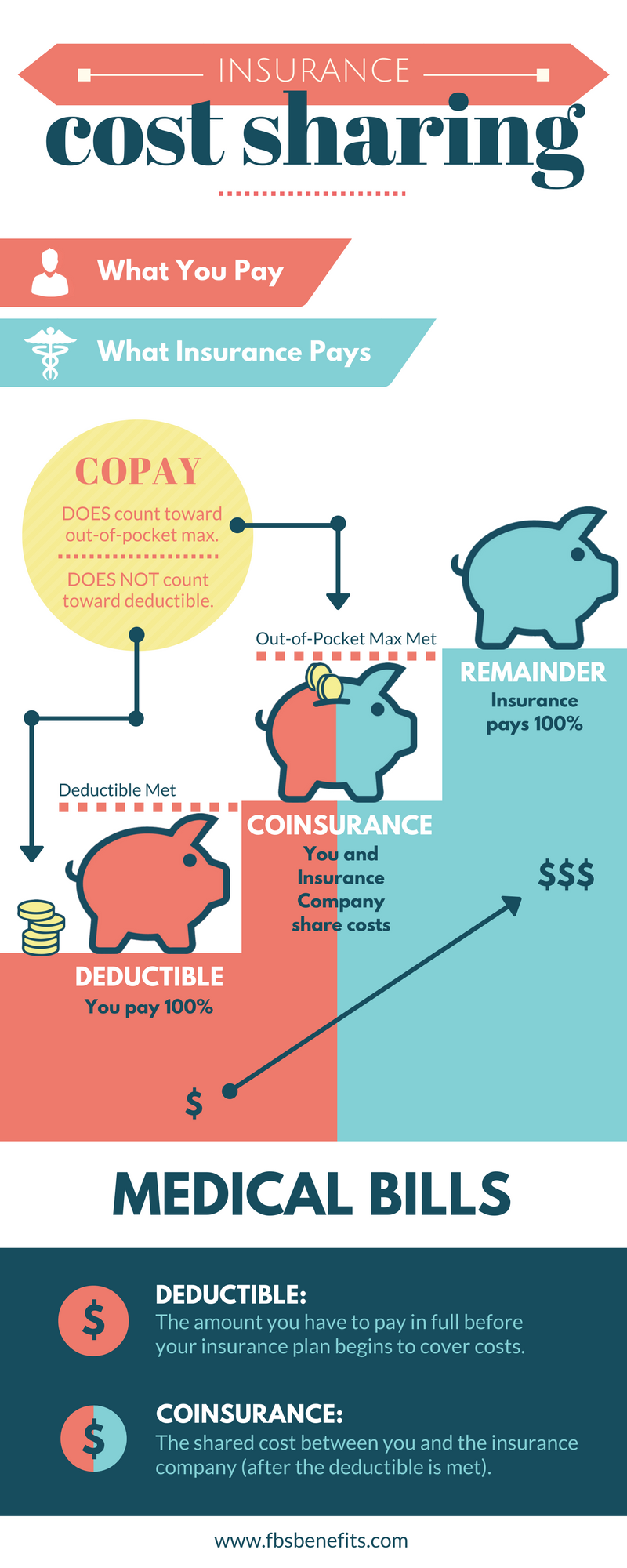

An insurance deductible is the predetermined amount of money that policyholders must pay out of their pocket before their insurance coverage kicks in. It is a form of self-insurance, where the policyholder takes on a portion of the risk by paying a deductible amount when filing a claim.

Types Of Insurance Deductibles

We have three types of insurance deductibles, they are

- Percentage-Based Deductibles

This insurance deductibles are calculated as a percentage of the total claim amount. For instance, if you have a health insurance policy with a 10% deductible and file a claim for $1,000, you would be responsible for paying $100 (10% of $1,000) before your insurance coverage begins.

- Flat-Rate Deductibles

Flat-rate deductibles is an insurance deductibles that involves a fixed amount which the policyholders pays as a most for each claim. For example, if you have auto insurance with a $3,000 flat-rate deductible and file a claim for $12,000, you would need to pay $3,000 before your insurance company covers the remaining $9,000.

- Progressive Deductibles

Progressive deductibles are often associated with comprehensive coverage. This deductible perform its work on a sliding scale, as the deductible amount increases based on the value of the insured property. For instance, just in homeowner’s insurance, the deductible is said to increas as the value of the home increases.

How Does An Insurance Deductible Work?

When an insurance claim is been made, the deductible amount is said to be subtracted from the total claim been payout. Let’s say you have an insurance policy on your house at $2,000 deductible, and you file a claim for $8,000 in damages. In this scenario, you would be responsible for paying the $2,000 deductible, while your insurance company would cover the remaining $6,000.

Note: In this method of deductible it is applicable to each separate claim you make in your insurance. For example, if you have a car insurance policy with a $1,000 deductible and you file two claims in a year, one for $5,000 and another for $6,000, you would need to pay the $1,000 deductible for each claim. This is because the insurance deductibles typically reset every year.

Why Do Insurance Policies Have Deductibles?

Insurance policies have deductibles for several reasons, some of the reasons are

- Deductibles helps in reducing the numbers of frivolous or small claims the policyholders may file. This can be achieved by asking the policyholders to make a contribution of a certain amount of money from the claims they made. While the insurance company can re-invest their resources to other important claims.

- Deductibles helps to arrange bothe interest of the policyholder and the insurer, by creating an avenue for responsible risk management. Whenever policyholders are incharge of deductible; they engages in reckless behavior as such causes calims.

- Insurance deductibles helps in keeping insurance premiums afforedable for everyone. This can be done through shifting some portion of the risks ro the policyholders and the insurers can give a lower costs in its coverage. However, higher deductibles generally correspond to lower premium amounts in insurance.

Factors To Consider When Choosing A Deductible

When selecting an insurance policy, you’ll often have the option to choose your deductible amount. It’s essential to consider the following factors before making a decision:

- Premiums vs. Deductibles

This two factors have an inverse relationship between premiums and deductibles. Higher deductibles usually result in lower premiums, while lower deductibles lead to higher premiums. Consider your budget and risk tolerance when determining the optimal balance between premium costs and deductible amounts.

- Risk Assessment

Evaluate the potential risks associated with the insured item or property. People living in an environmnet that often have natural disasters, like hurricanes, flood or earthquakes, opting for a lower deductible might be advantageous. Conversely, if the risk of damage or loss is relatively low, you might consider a higher deductible to save on premium costs.

- Affordability

Ensure that the chosen deductible amount is affordable for you in the event of a claim. You should be comfortable paying the deductible without causing financial strain. Assess your financial situation and select a deductible that aligns with your ability to cover the cost.

- Claiming an Insurance Deductible

Understanding the process of claiming an insurance deductible is crucial to ensure a smooth experience when filing a claim. Here are the key steps involved:

- Meeting the Deductible

Before your insurance coverage begins, you must meet your deductible by paying the required amount out of pocket. Ensure you have the necessary funds available to cover the deductible when filing a claim.

- Submitting a Claim

Contact your insurance provider to initiate the claims process. Provide all the required information, including details of the incident or damage, supporting documents, and any relevant photographs or evidence.

- Reimbursement Process

After the claim is processed and approved, the insurance company will reimburse you for the covered amount minus the deductible. Be sure to review the terms and conditions of your policy to understand the timeline and procedure for reimbursement.

Pros And Cons Of High And Low Deductibles

Both high and low deductibles have their own advantages and disadvantages. Consider the following:

- High Deductibles

Pros:

– Lower premiums: Opting for a higher deductible generally leads to lower premium costs, allowing you to save money on your insurance policy.

– Financial control: By taking on a larger portion of the risk, you have more control over your insurance expenses.

– Ideal for low-risk situations: If you have a low-risk profile or can afford to cover higher out-of-pocket costs, a high deductible can be a suitable choice.

Cons:

– Financial burden: In the event of a claim, a high deductible may place a significant financial burden on you, requiring a substantial amount of money upfront.

– Limited coverage for small claims: With a high deductible, you may not be able to claim for smaller or more frequent damages, as the cost of repair or replacement may fall below the deductible threshold.

– Higher out-of-pocket expenses: Until you meet the high deductible, you are responsible for covering the full cost of any claims.

- Low Deductibles

Pros:

Lower out-of-pocket costs: With a low deductible, you have lower upfront expenses when filing a claim.

Coverage for smaller claims: A low deductible allows you to claim for smaller damages that may not exceed the deductible amount.

Greater peace of mind: Knowing that you have minimal financial responsibility for claims can provide a sense of security.

Cons:

Higher premiums: A low deductible typically comes with higher premium costs, as the insurer assumes more of the risk.

Less financial control: You have less control over the cost of your insurance policy since a larger portion of the risk is transferred to the insurer.

Potentially unnecessary claims: With a low deductible, there may be a temptation to file claims for minor damages that you could afford to pay for out of pocket.

Conclusion

In conclusion, understanding insurance deductibles is crucial for navigating the world of insurance and making informed decisions. Deductibles play a crucial role in managing risk and determining the cost of insurance policies. By carefully considering factors such as affordability, risk assessment, and the pros and cons of high and low deductibles, you can select a deductible amount that aligns with your needs and financial situation. Remember to review your policy terms, assess your financial situation, and consult with professionals when needed.