In the realm of insurance, collision insurance plays a vital role in safeguarding your vehicle against the unforeseen. Whether you’re a new driver or an experienced one, understanding collision insurance is crucial for protecting your investment. This article will provide an in-depth overview of collision insurance, its coverage, benefits, and considerations. So, let’s delve into the world of collision insurance and explore how it can offer peace of mind on the road.

Understanding Collision Insurance

Collision insurance is a type of auto insurance coverage that protects your vehicle in the event of a collision with another vehicle, object, or a single-vehicle accident. Unlike liability insurance, which covers damages caused to others, collision insurance covers the repair or replacement costs for your vehicle, regardless of fault. It provides coverage for both accidents involving other vehicles and accidents involving fixed objects, such as trees or utility poles.

How Does Collision Insurance Work?

When you have collision insurance, and your vehicle is involved in an accident, the insurance company will reimburse you for the repair costs or the actual cash value (ACV) of your vehicle if it’s deemed a total loss. The ACV is the market value of your vehicle at the time of the accident, taking into account factors such as depreciation.

To initiate a claim, you must notify your insurance company promptly and provide them with all the necessary details and documentation. An adjuster will assess the damage and determine the amount to be paid out, considering the deductible and the coverage limits outlined in your policy.

Coverage Provided By Collision Insurance

Collision insurance primarily covers the costs associated with repairing or replacing your vehicle after a collision. This includes damages resulting from accidents with other vehicles, accidents with objects, or rollovers. The coverage extends to both at-fault and not-at-fault accidents, providing you with financial protection regardless of who is responsible for the collision.

It’s important to note that collision insurance typically does not cover medical expenses or damages to other people’s property. For those types of expenses, you would need additional coverage, such as bodily injury liability or property damage liability insurance.

Collision Insurance Deductibles

When purchasing collision insurance, you’ll need to choose a deductible amount. The deductible is the portion of the repair costs that you’re responsible for paying out of pocket before your insurance coverage kicks in. For example, if you have a $500 deductible and the repair costs amount to $2,000, you would pay $500, and your insurance company would cover the remaining $1,500.

Choosing a higher deductible can lower your collision insurance premiums, but it also means you’ll have a higher out-of-pocket expense in the event of an accident. Conversely, selecting a lower deductible will result in higher premiums but reduce your financial burden at the time of a claim.

Factors Affecting Collision Insurance Premiums

1. Vehicle Type and Value: The make, model, and value of your vehicle play a significant role in determining your collision insurance premiums. Expensive or luxury vehicles typically have higher premiums due to the higher repair or replacement costs.

2. Driving Record: Your driving history and record of accidents or traffic violations can impact your collision insurance rates. A clean driving record with no accidents or tickets may qualify you for lower premiums.

3. Deductible Amount: As mentioned earlier, the deductible you choose affects your premiums. Higher deductibles usually result in lower premiums, while lower deductibles lead to higher premiums.

4. Location: The area where you reside and primarily drive can affect your collision insurance rates. Urban areas with higher traffic and accident rates may have higher premiums compared to rural areas.

5. Age and Experience: Young and inexperienced drivers often face higher collision insurance premiums due to the higher risk associated with their age group. As you gain driving experience and maintain a clean record, your premiums may decrease.

6. Credit History: In some states, insurance companies may consider your credit history when determining your premiums. A good credit score can result in lower rates.

It’s important to compare quotes from different insurance providers to find the best coverage and premiums that suit your needs and budget.

The Importance Of Collision Insurance

Collision insurance is essential for protecting your vehicle investment. Accidents can happen unexpectedly, and repairing or replacing a damaged vehicle can be costly. Collision insurance provides financial security by covering these expenses, allowing you to restore your vehicle to its pre-accident condition without bearing the full financial burden.

Additionally, if your vehicle is financed or leased, collision insurance is often required by the lender or lessor. It ensures that the vehicle’s value is protected, and the loan or lease terms are satisfied in the event of an accident.

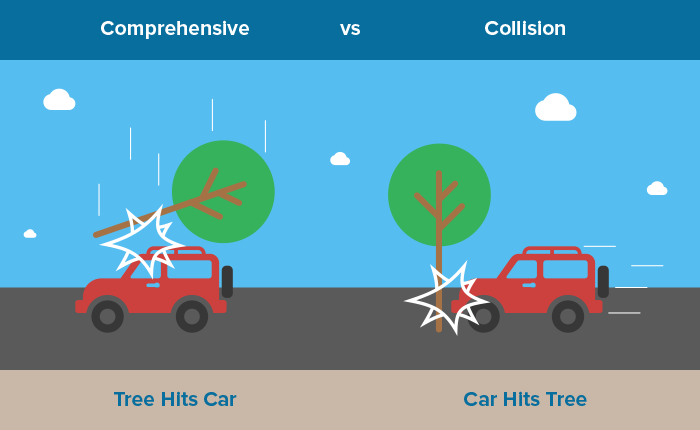

Collision Insurance Vs. Comprehensive Insurance

It’s worth noting the difference between collision insurance and comprehensive insurance. While collision insurance covers damages resulting from accidents, comprehensive insurance provides coverage for non-collision incidents, such as theft, vandalism, fire, natural disasters, and encounters with animals.

Both collision and comprehensive insurance are optional coverages, but they can offer comprehensive protection when combined. Assessing your needs and the value of your vehicle will help determine whether one or both coverages are necessary for you.

When Do You Need Collision Insurance?

Collision insurance is most beneficial for newer vehicles or vehicles with a higher value. If you have an older vehicle with a low market value, the cost of collision insurance may outweigh the potential benefits. In such cases, it may be more cost-effective to allocate the funds toward a new vehicle rather than paying premiums for collision coverage.

However, if your vehicle holds significant value or you rely heavily on it for daily transportation, collision insurance is highly recommended. It provides peace of mind and financial protection against unexpected accidents.

Choosing The Right Collision Insurance Policy

When selecting a collision insurance policy, it’s crucial to consider the following:

1. Coverage Limits: Ensure that the policy provides sufficient coverage to repair or replace your vehicle based on its current market value.

2. Deductible Options: Choose a deductible amount that aligns with your budget and risk tolerance.

3. Insurance Provider Reputation: Research and compare insurance companies to find a reputable provider with good customer service and a track record of efficiently handling claims.

4. Policy Exclusions and Limitations: Read the policy terms and conditions carefully to understand any exclusions or limitations that may affect your coverage.

By evaluating these factors and consulting with insurance professionals, you can make an informed decision and select the collision insurance policy that best suits your needs.

Collision Insurance Claims Process

When it comes to filing a collision insurance claim, it’s essential to follow the proper steps to ensure a smooth process:

1. Contact your insurance company: Notify your insurance provider as soon as possible after the accident. Provide them with accurate and detailed information about the incident, including the date, time, location, and any relevant documentation, such as the police report or photographs of the damage.

2. Work with an adjuster: Your insurance company will assign an adjuster to assess the damage to your vehicle. They will evaluate the repairs needed and estimate the cost of repairs or the actual cash value (ACV) if your vehicle is deemed a total loss.

3. Obtain repair estimates: You may be required to obtain repair estimates from authorized repair shops or garages. These estimates will help determine the amount of coverage provided by your collision insurance.

4. Pay your deductible: If your claim is approved, you will need to pay your deductible amount to the repair shop before they begin work on your vehicle. The insurance company will cover the remaining costs, up to your coverage limits.

5. Vehicle repair or replacement: Once the claim is processed, you can proceed with the repairs or, in the case of a total loss, discuss the options for vehicle replacement with your insurance company.

6. Follow-up and documentation: Keep track of all communication with your insurance company, repair shop, and any other involved parties. Document any additional expenses incurred as a result of the accident, such as towing or rental car fees.

By following these steps and maintaining open communication with your insurance provider, you can navigate the collision insurance claims process more efficiently.

Conclusion

Collision insurance is an important component of auto insurance that protects your vehicle from the financial impact of accidents and collisions. It covers repair costs or provides compensation for a total loss, ensuring that you can get back on the road without incurring significant expenses. By understanding collision insurance, its coverage, and the claims process, you can make informed decisions to protect your vehicle investment and enjoy peace of mind while driving.